A cause for optimism for the future of Islamic finance

-

George Mickhail Available: The Jakarta Post

The share of cross-border investment in the world in 2016 accounted for less than 10 percent of all investment in the world, according to the latest DHL Interconnectedness Index. (Shutterstock/File)

The gross global cross-border capital flows comprise the annual foreign capital inflows and outflows between a country and the rest of the world. The Islamic participation, by way of the share of Shari’ah complaint instruments, in any of those types of flows, is what may be considered as global Islamic cross-border capital flows.

There are, however, fundamental challenges to its measurement, due to limitations imposed by authenticity, availability and heterogeneity when collecting national data, grey-markets in money transfers, and multinational transfer pricing across borders.

Furthermore, the disparity of country membership in global institutions, like the IMF, BIS and the IFSB, and the variability of reporting timelines to those institutions has made it difficult to reconcile the data reported to empirically determine a ‘reliable value’ of cross-border capital flows from the gross value of the global Islamic financial services industry (IFSI).

The McKinsey Global Institute (MGI) reported that gross global cross-border capital flows have shrunk by 65 percent from US$12.4 trillion in 2007 to $4.3 trillion in 2016. Half of that decline reflects a sharp reduction in cross-border lending and other banking activities in the Eurozone.

The gross global financing assets in 2016, were about $132 trillion, and the global cross-border flows were $4.3 trillion or the equivalent to 3.3 percent of all financial assets.

In contrast, the IFSB reported that the global assets of the gross value of the global Islamic financial services industry (IFSI) in 2016 were ‘estimated’ at $1.9 trillion as of November 5, 2017, and included: Islamic Banking ($1.5 trillion for the 6 months ended June 2016), Sukūk outstanding ($318.5 billion for the full-year 2016), Islamic Funds Assets ($56.1 billion for the full-year 2016), and Takāful ($25.1 billion as at the end of 2015). Accordingly, the global IFSI assets represent approximately 1.4 percent of the global financing assets.

Then, if we assume that the global Islamic cross-border financing flows would follow the same pattern as global cross-border capital flows, then an equivalent 3.3 percent of all Islamic financial assets would be approximately $62.7 billion.

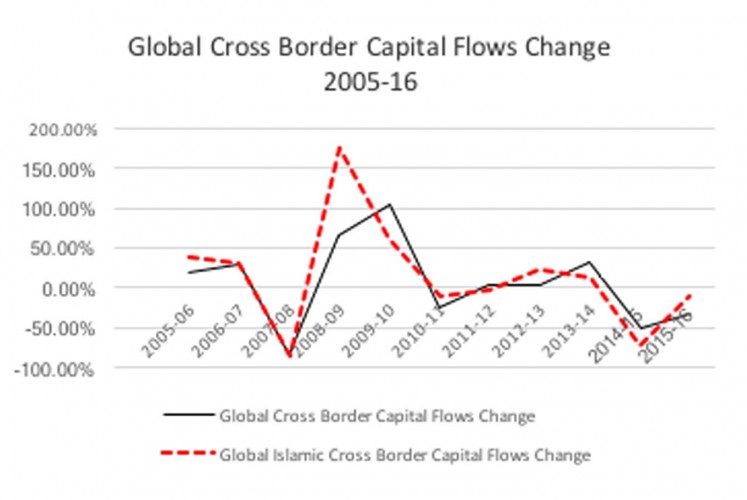

To confirm this conjecture, an examination of the IMF Balance of Payments statistics for the 2005-16 period was carried out to determine the Islamic portion of global cross-border capital flows according to the historical Islamic participation rates in cross-border banking and finance (GCC 34 percent, ASEAN 13 percent, Southeast Asia 12 percent, and Turkey, Jordan, Egypt, Sudan and South Africa 6 percent). The analysis revealed that this ‘rudimentary’ calculation was understating the steady growing share of global Islamic cross-border capital flows of the gross global cross-border capital flows, which were approximately $335.8 billion or 3.3 percent of the global gross cross-border capital flows in 2005; growing to $603.7 billion (6.3 percent) in 2013, then falling to $109.5 billion (4 percent) in 2016.

10 year Change in Global Islamic Cross Border Capital Flows (George Mickhail/File)

10 year Change in Global Islamic Cross Border Capital Flows (George Mickhail/File)

The gross global Islamic cross-border capital flows have declined by 73 percent during 2014-15 and 10.2 percent during 2015-16, which was similar to the decline in the gross global cross-border capital flows over the last couple of years, falling by -51.1 percent during 2014-15 and 32.1 percent during 2015-16.

No doubt, the historically low-oil prices with geopolitical instability in the aftermath of the Arab Spring, and the rise of economic and anti-Islamic nationalists in Europe and elsewhere under the pretext of the ISIS terror threat and the European refugee crisis, have contributed to a diminishing appetite for Islamic Banking and Finance (IBF) as they have to contend with serious “reputational risk” pressures to their bottom lines.

In contrast, there is cause for optimism with the powerful forces of global Muslim population growth; emerging economies growing faster than advanced economies; rising affluence and economic participation; increased demand for ethical investments; rise in Islamic financial centres; sophistication of Shari’ah compliant finance; harmonization and integration of Islamic financial practices to global accounting and risk management standards; and Sukūk issuance is rapidly growing globally.

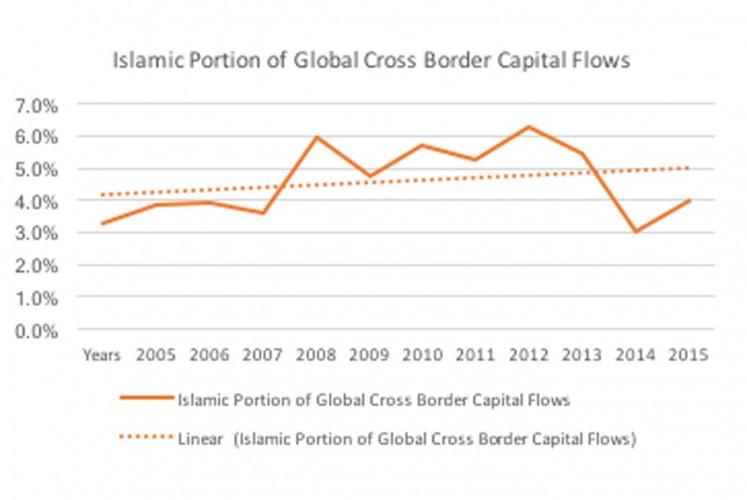

One particular powerful force that is of note, is Hong Kong becoming the first ‘AAA’-rated government in the world, to issue a dollar-denominated Sukūk (three worth $3 billion were issued since September 11, 2014). The issuance of Sūkuk and Sharia’ah compliant financial instruments must be viewed within the context of financing the infrastructure needs of China’s One Belt, One Road (OBOR) strategic economic partnership with its historical ‘silk road’ partners across Eurasia, where 40 percent of OBOR countries are Muslim. Recent developments in the Middle East and Southeast Asia, that are an extension of some of these forces offer a great cause for optimism that is nonetheless supported empirically by a trend incline since 2005 in the Islamic share of cross-border transactions (Graph 2).

Islamic Portion of Global Cross Border Capital Flows (2005-2016) (George Mickhail/File)

Islamic Portion of Global Cross Border Capital Flows (2005-2016) (George Mickhail/File)

On Oct. 22, 2017, the Saudi Arabian Monetary Agency joined AAOIFI, which promises to boost cross-border deals. While, on November 3, 2017, a digital free trade zone (DFTZ), which is the brainchild of Jack Ma of Alibaba, went live enabling more than 2,000 Malaysian SMEs to capitalize on cross-border e-commerce activities. The Malaysian digital free trade zone, capitalizes on the rise of FinTech, machine learning and Blockchain technology, which would enable lower-cost, more secure Islamic cross-border financing flows. Furthermore, P2P lending, funding and payments platforms may broaden global participation in Islamic banking and finance. On the other hand, RegTech platforms may be used to manage risks associated with Islamic cross-border capital flows.

The evolution of the Islamic finance industry into a more sustainable ecosystem with over 1,291 financial institutions in more than 85 countries, means that it can contribute to the economic development of emerging economies of which many are Muslim, and profit-sharing diplomacy for global players seeking to advance their interests in Africa, the Middle East, Europe and Southeast Asia.

These initiatives are taking place against the $1 trillion investment by China in its bold, innovative and strategic OBOR project that is spanning more than 68 countries and 4.4 billion people that collectively comprise 40 percent of the global GDP.

To date, more than 25 member countries of the Organisation of Islamic Countries (OIC) have joined the OBOR initiative, while 22 Arab countries have various agreements and treaties with China. Currently, China is the largest single trading partner for the OIC bloc, and the second largest for Arab countries as a whole. China’s OBOR long-term strategic project offers an infrastructure backbone of maritime, land and digital trade, which would accelerate the global growth in cross-border trade and finance.

In conclusion, the OBOR geo-economic initiative coupled with technological innovations in global Islamic cross-border trade and finance certainly promises considerable growth in 2018 and beyond.

***

George is an LSE trained Egyptian-born Australian, who holds visiting professorships at a number of business schools in France concurrently with his permanent appointment at the University of Wollongong, which he joined after a few years at the University of Sydney. Reach him via LinkedIn, Twitterand email george@uow.edu.au